Nayuki became a penny stock. The real lesson is not the empty AGM.

Nayuki's fall from a HK$19.80 IPO price to below HK$1 is a useful case study in what happens when a premium consumer story meets store economics, delivery habits, and harder profit math.

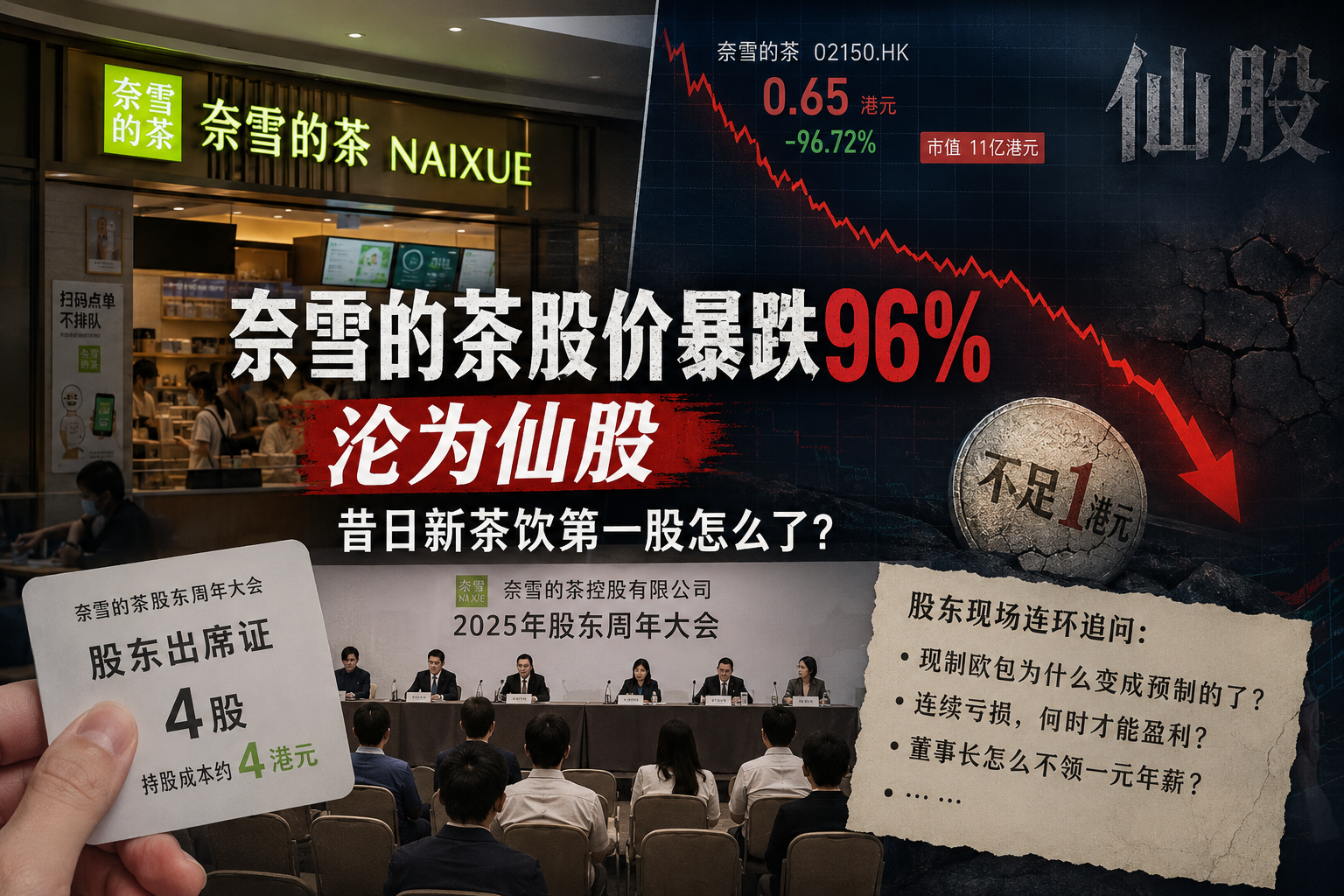

Buying four shares for roughly HK$4, walking into a listed company's annual meeting, and joking that two free drinks already covered the cost sounds like internet theater. It stings because the company was once sold to the market as the premium face of China's new tea-drink boom.

Nayuki's problem is not only that its share price has fallen from a HK$19.80 IPO price to around HK$0.65, or that it now trades below HK$1. The larger signal is this: when a consumer brand builds its valuation on large stores, fresh-baked bread, lifestyle spaces, and a capital-market growth story, the story can deflate fast once customers move to delivery, price pressure rises, and store economics become harder to hide.

The AGM was the hook, not the whole story

National Business Daily reported on July 2, 2026 that a young retail shareholder attended Nayuki's annual general meeting after buying only a few odd-lot shares. The report also described a small number of shareholders on site, including some with large paper losses, asking about losses, store costs, pre-prepared bakery products, executive compensation, and share buybacks.

Those meeting-room details come from media interviews and attendee recollections, not from the company's formal disclosure. What can be verified from official filings is narrower but important: Nayuki did hold its annual general meeting on June 24, 2026, the relevant resolutions passed, and the company's 2025 annual results still showed a loss.

So the sparse meeting is the emotional doorway. The financial structure is the actual story.

From HK$19.80 to HK$0.65: what the market is repricing

Nayuki listed in 2021 with an offer price of HK$19.80 per share. Using the HK$0.65 level cited in the media report, the stock is down roughly 96.7% from that IPO price. That is not a normal pullback. It is the market taking a "premium new tea growth stock" and forcing it back into the older language of cash flow, store efficiency, and durable profit.

The 2025 numbers show why:

| Metric | 2025 result | What it suggests |

|---|---|---|

| Revenue | RMB4.3312 billion, down about 12.0% year over year | Growth narrative weakened |

| Net loss | RMB243.5 million | Losses narrowed but did not disappear |

| Adjusted net loss | RMB240.5 million, adjusted loss margin of 5.6% | Cost work helped, but profitability is still pending |

| Average order value in self-operated stores | RMB24.4, down from RMB26.7 in 2024 | Premium pricing power is under pressure |

| Revenue mix in self-operated stores | Delivery 52.6%, pickup 38.1%, in-store counter orders 9.3% | The "third place" value needs to be repriced |

The market used to ask whether Nayuki could become a Starbucks-like premium tea space. Now it is asking a simpler question: in delivery platforms, mall stores, and franchised smaller formats, which model actually earns money?

The awkward part: the brand still exists, but the scene changed

Nayuki is not a company with no assets. It still has brand awareness, supply-chain capability, members, stores, and liquidity. At the end of 2025, it reported roughly RMB1.5851 billion in cash and cash equivalents, RMB1.0725 billion in term deposits and certificates of deposit, and no bank loans.

That makes the case more interesting. This is not a simple "running out of cash" story. It is a brand with resources trying to adapt after the consumption scene moved underneath it.

The large-store logic was: customers enter the store, sit down, take photos, buy tea, add bakery items, and buy into a lifestyle. Delivery logic is different: price, speed, flavor consistency, coupons, and platform exposure matter more.

Once delivery accounts for more than half of self-operated store revenue, Nayuki has to answer tougher questions. How large should stores be if customers no longer stay? If bakery shifts toward cold-chain reheating, what still makes the brand feel different? If franchising carries expansion, how does the company protect traffic, service, and quality?

Shareholder questions are really customer questions

The sharp questions in the report look like shareholder questions: Why is the company still losing money? Why not link executive pay more directly to performance? Why did the bakery experience change? Why have buybacks not fixed the stock price?

Translated into customer language, they become more familiar:

- Is the "more premium" Nayuki I used to like still worth paying extra for?

- If stores get smaller and bakery becomes more standardized, what is meaningfully different from other tea chains?

- If discounts and delivery become the main gateway, will I choose the brand for love or for price?

- If management says optimization is working, when will it show up in both profit and experience?

That is the brutal part of consumer stocks. Investors can read filings; customers only judge the next order. Cost optimization may improve the income statement, but if it makes the cup, bread, store, or service feel downgraded, the brand pays for it later.

Why this matters beyond one tea chain

If you are just a tea-drink customer, the lesson is simple: a brand rarely moves from "expensive but worth it" to "only worth it with a coupon" overnight. The shift usually leaks out through store size, serving format, discount frequency, product feel, and small service details.

If you build products, content, or consumer businesses, Nayuki is a sharper case study:

- Premium positioning needs repeatable proof, not only early storytelling.

- Big stores, big teams, and complex supply chains eventually return to unit economics.

- When user behavior moves online, a brand must rebuild differentiation instead of merely moving the old model onto platforms.

- Cost reduction can help the P&L, but it must not teach core users that the experience has been downgraded.

The line worth remembering is this: a consumer brand should not fear discounting as much as it should fear becoming recognizable only by the discount.

What to watch next

Nayuki still has cards to play. The question is whether it can prove three things:

- Smaller stores, franchising, overseas growth, and delivery can create stable profit instead of just adding management complexity.

- Bakery, light meals, ready-to-drink products, and the core tea line can rebuild differentiation rather than distract from one another.

- Beyond buybacks and market-value management, operating data can improve for several reporting periods in a row.

As of July 3, 2026, the most useful question is not whether Nayuki can return to HK$19.80. It is whether the company can show it no longer depends on the old story.

An annual meeting can be quiet. A stock price can be depressed. What cannot go quiet is the customer's reason to order again.

Sources

Related

Sonnet 5 is not just a friendly price cut. It is Anthropic's answer to developer cost anxiety, account-enforcement frustration, and the pressure to make agents run at scale. Claude is still powerful, but platform trust is becoming the real bottleneck.

A Chinese report says Alibaba has told employees to uninstall Claude and Claude Code. The internal ban itself is not publicly confirmed, but Anthropic's China restrictions, distillation accusations, Claude Code marker controversy, and the U.S. 1260H list all point to the same lesson: AI coding tools are now supply-chain risk, not just productivity software.